Cash surrender nonforfeiture options play a crucial role in the world of life insurance, providing policyholders with a safety net should they choose to discontinue their policy. These options ensure that policyholders do not lose all their invested premiums if they decide to surrender their policy before its maturity. With an increasing number of individuals seeking to understand their insurance options, this article delves into the intricacies of cash surrender nonforfeiture options, their benefits, and the implications for policyholders.

The cash surrender value is the amount of money an insurance company will pay to the policyholder if they decide to cancel their policy. This feature is particularly relevant for whole life and universal life insurance policies. Understanding how these options work can help individuals make informed decisions about their life insurance investments. This article will explore the various aspects of cash surrender nonforfeiture options, including how they function, their benefits, and potential drawbacks.

In this guide, we will cover the essential elements of cash surrender nonforfeiture options, their significance in life insurance policies, and what policyholders should consider when evaluating these options. Whether you are a seasoned insurance buyer or new to the concept, this article aims to provide valuable insights and practical information.

Table of Contents

- What is a Nonforfeiture Option?

- Types of Nonforfeiture Options

- Cash Surrender Value Explained

- Benefits of Cash Surrender Options

- Drawbacks of Cash Surrender Options

- How to Access Cash Surrender Value

- Considerations Before Surrendering Your Policy

- Conclusion

What is a Nonforfeiture Option?

A nonforfeiture option is a provision within a life insurance policy that allows the policyholder to retain some value if they decide to discontinue the policy. This ensures that even if the policyholder stops paying premiums, they will not lose all the benefits they have accumulated. The most common nonforfeiture options include cash surrender value, reduced paid-up insurance, and extended term insurance.

Types of Nonforfeiture Options

There are several types of nonforfeiture options available for policyholders, including:

- Cash Surrender Value: The amount the policyholder receives if they choose to cancel their policy.

- Reduced Paid-Up Insurance: A policy option where the policyholder can convert their existing policy into a new one with a lower face value but no further premium payments required.

- Extended Term Insurance: This option allows the policyholder to use the cash value of their policy to purchase a term policy with the same death benefit for a specific period.

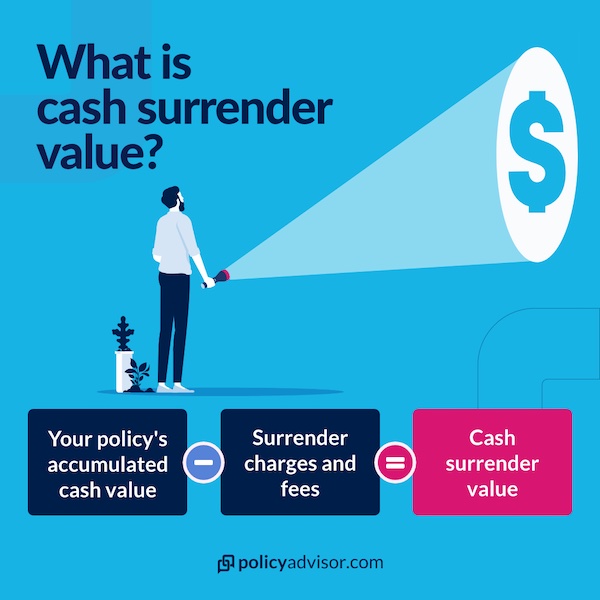

Cash Surrender Value Explained

The cash surrender value is a critical component of cash surrender nonforfeiture options. It is the amount of money that the insurance company will pay to the policyholder upon surrendering their policy. The cash surrender value typically accumulates over time as the policyholder pays premiums, and it is influenced by factors such as:

- The type of policy (whole life, universal life, etc.)

- The length of time the policy has been active

- The total premiums paid into the policy

- Any loans or withdrawals taken against the policy

Benefits of Cash Surrender Options

Cash surrender nonforfeiture options offer several advantages, including:

- Financial Flexibility: Policyholders can access cash value instead of losing all investments if they choose to discontinue their policy.

- Emergency Fund: The cash surrender value can serve as an emergency fund, providing liquidity when needed.

- Reduced Debt: The funds can be used to pay off debts or cover unexpected expenses.

Drawbacks of Cash Surrender Options

Despite the benefits, there are also drawbacks to consider:

- Loss of Coverage: Surrendering the policy means losing life insurance coverage.

- Tax Implications: Depending on the amount received, there may be tax consequences for the policyholder.

- Reduced Death Benefit: If the policyholder opts for reduced paid-up insurance, the death benefit may be significantly lower.

How to Access Cash Surrender Value

Accessing the cash surrender value typically involves the following steps:

- Contact your insurance provider and request a cash surrender value quote.

- Complete any necessary paperwork as required by the insurance company.

- Receive the cash surrender value, usually via check or direct deposit.

Considerations Before Surrendering Your Policy

Before deciding to surrender your life insurance policy, consider the following:

- Evaluate your financial needs and whether you truly need to access the cash value.

- Consider the long-term implications of losing your life insurance coverage.

- Consult with a financial advisor to understand the best course of action.

Conclusion

In summary, cash surrender nonforfeiture options provide policyholders with critical financial flexibility and a way to recover some value from their life insurance policies. However, they come with potential drawbacks that must be carefully weighed. It's essential to understand these options fully and consider your unique financial situation before making any decisions. We encourage readers to leave comments or questions below and explore more articles for a deeper understanding of financial planning.

Thank you for reading! We hope this article has provided valuable insights into cash surrender nonforfeiture options. Be sure to return for more informative content on insurance and financial planning.

You Might Also Like

Colorado Football On TV: Your Ultimate Guide To Watching The BuffaloesUltimate Guide To Retro Fitness Hoboken, NJ: Your Path To A Healthier Lifestyle

UCF Football Live: Experience The Thrill Of College Football In Real Time

Exploring Gotham City: The Heart Of New Jersey's Urban Culture

Discovering Six Brothers Diner: A Culinary Gem In Little Falls, NJ

Article Recommendations

- Orlando Freefall Accident 2024

- Rivian R1t Range

- Snoop Dog Threatens Donal Trump

- Patrick Mahomes Rc

- Tom Byron And Traci Lords

- Bash In Berlin 2024 Predictions

- People Magazine Archive

- Lilydaisyphillips

- Patricia Arquette Net Worth

- Faye Dunaway Net Worth 2024