Understanding no fault states for car accidents is essential for drivers across the United States. These laws significantly impact how insurance claims are handled and can affect your financial responsibilities after an accident. In no fault states, the process of seeking compensation for vehicle accidents is streamlined, allowing for quicker resolutions. This article will delve into the intricacies of no fault insurance, the states that implement these laws, and how they can affect you as a driver.

As the number of vehicles on the road continues to rise, so does the likelihood of accidents. No fault insurance laws aim to simplify the claims process and reduce litigation. However, the specifics of these laws can vary significantly from one state to another. Understanding the nuances will help you make informed decisions regarding your auto insurance and your rights following an accident.

In this comprehensive guide, we will explore the definition of no fault insurance, list the states that have adopted these laws, and provide insights into how they function. We will also examine the pros and cons of no fault states for car accidents, helping you to navigate this complex subject with ease.

Table of Contents

- What is No Fault Insurance?

- List of No Fault States

- How No Fault Insurance Works

- Pros and Cons of No Fault Insurance

- Exceptions to No Fault Laws

- Impact on Drivers in No Fault States

- Choosing Auto Insurance in No Fault States

- Conclusion

What is No Fault Insurance?

No fault insurance is a type of auto insurance policy that allows drivers to receive compensation for their injuries and damages without having to establish who was at fault for the accident. This system is designed to streamline the claims process and minimize the need for litigation.

In no fault states, each driver's insurance company pays for their policyholder’s medical expenses and damages, regardless of who caused the accident. This means that you can receive compensation for medical bills, lost wages, and other expenses without having to prove that the other driver was at fault.

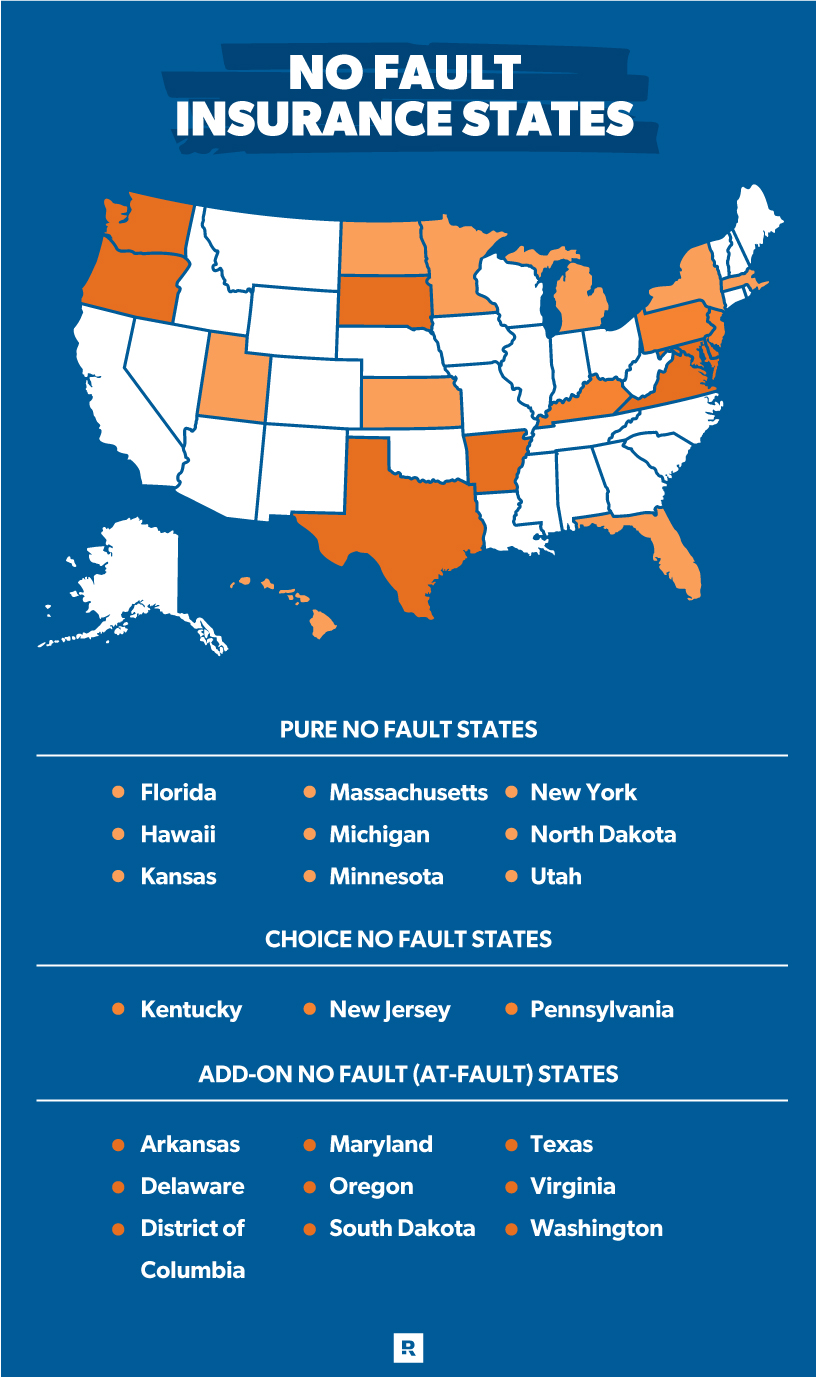

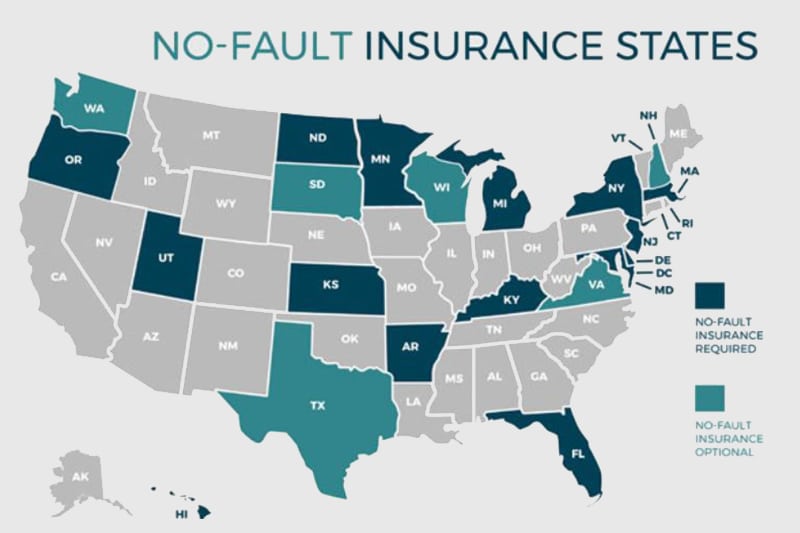

List of No Fault States

As of now, the following states in the U.S. operate under no fault insurance laws:

- Florida

- Michigan

- New York

- New Jersey

- Pennsylvania

- Hawaii

- Massachusetts

- Kentucky

- North Dakota

- Utah

How No Fault Insurance Works

In a no fault insurance system, drivers are required to carry personal injury protection (PIP) coverage. This coverage pays for medical expenses, rehabilitation costs, and lost wages. Here’s how it typically works:

- After an accident, each driver files a claim with their own insurance company.

- The insurance company pays for the policyholder's medical expenses and lost wages up to the policy limits.

- In most cases, drivers cannot sue each other for damages unless the injuries meet a certain threshold.

Thresholds in No Fault States

Some no fault states have thresholds that must be met before a driver can file a lawsuit against the at-fault driver. These thresholds can be based on:

- Severity of injuries

- Medical expenses

- Loss of income

Pros and Cons of No Fault Insurance

Pros of No Fault Insurance

- Faster claims processing

- Reduced litigation costs

- Less stressful for drivers

Cons of No Fault Insurance

- Limited ability to recover damages

- Higher insurance premiums in some states

- Potential for inadequate compensation for serious injuries

Exceptions to No Fault Laws

While no fault laws simplify the claims process, there are exceptions where a driver can seek additional compensation through litigation. These exceptions may include:

- Severe injuries that meet a certain threshold

- Accidents involving uninsured or underinsured motorists

- Intentional acts or reckless driving

Impact on Drivers in No Fault States

Living in a no fault state can significantly impact your insurance choices and your rights after an accident. Here are some key considerations:

- Insurance premiums may be higher due to mandated PIP coverage.

- Drivers may feel more secure knowing that their medical expenses will be covered regardless of fault.

- Understanding your rights and the limitations of no fault coverage is crucial for making informed decisions.

Choosing Auto Insurance in No Fault States

When selecting an auto insurance policy in a no fault state, consider the following tips:

- Compare PIP coverage options to ensure adequate protection.

- Research the insurance company's reputation and customer service ratings.

- Review state-specific regulations regarding claims and coverage limits.

Conclusion

In summary, understanding no fault states for car accidents is crucial for every driver. These laws can simplify the process of receiving compensation after an accident, but they also come with their own set of complexities and limitations. By familiarizing yourself with no fault insurance, the states that implement it, and the pros and cons associated with it, you can make informed decisions about your auto insurance coverage.

We encourage you to leave a comment below with your thoughts on no fault states or share this article with fellow drivers who may benefit from understanding these laws. Additionally, explore our other articles for more insights into auto insurance and road safety.

Thank you for reading! We hope to see you back for more informative content.

You Might Also Like

Is Colonial Penn Life Insurance Good? A Comprehensive ReviewComplete Guide To NJ Driver Registration: Everything You Need To Know

Will Kelce Play Tonight? A Comprehensive Analysis

What Color Lipstick Does Taylor Swift Wear? Discover Her Iconic Shades

Understanding Business Hazard Insurance: Protecting Your Business From Unforeseen Risks

Article Recommendations

- Whats In A Big Mac

- Dylan Scott Net Worth

- Movierulz 2024 Page 2

- Stream Wwe

- David Duchovny And Gillian Anderson

- Girlfriend Found Dead

- Selena Quintanilla Portrait

- Patricia Belcher Husband

- Kelly Jane Caron Onlyfans Leaks

- Travis Barker Melissa Kennedy